United States Paper Packaging Market Overview

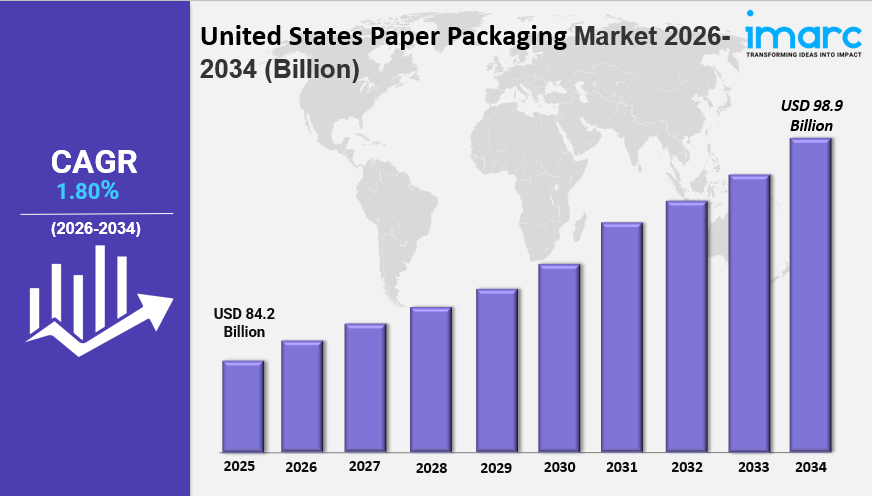

The United States paper packaging market is on a steady growth trajectory, driven by rising environmental concerns, the rapid expansion of e-commerce, and stringent government regulations promoting sustainable packaging alternatives. Valued at USD 84.2 Billion in 2025, the market is projected to reach USD 98.9 Billion by 2034, exhibiting a CAGR of 1.80% during 2026–2034. Growth is powered by increasing demand for recyclable and eco-friendly packaging solutions, surging online retail activity, and expanding applications across the food, beverage, healthcare, and personal care industries.

Access In-Depth Market Intelligence — Download Your Free Sample Copy: https://www.imarcgroup.com/united-states-paper-packaging-market/requestsample

Key Market Statistics at a Glance

- Base Year: 2025

- Historical Years: 2020–2025

- Forecast Period: 2026–2034

- Market Size (2025): USD 84.2 Billion

- Projected Size (2034): USD 98.9 Billion

- Growth Rate: CAGR of 1.80%

- Leading Region: South (Largest market in 2025)

United States Paper Packaging Market Growth Trends

• Rising Environmental Concerns and Sustainability Mandates Growing awareness about plastic pollution and the environmental impact of non-biodegradable packaging is one of the primary drivers of the paper packaging market. Consumers, brands, and retailers are actively shifting toward paper-based alternatives, and this transition is reinforced by corporate sustainability pledges and increasing pressure from environmental advocacy groups.

• Stringent Government Regulations and Policy Support The implementation of stringent federal and state-level regulations by the U.S. Government is actively promoting the adoption of paper-based packaging to minimize pollution and reduce toxic waste levels. Policies targeting the reduction of single-use plastics and encouraging recyclable materials are directly benefiting the paper packaging industry.

• Surge in E-Commerce and Online Retail Activity The continued expansion of online shopping platforms is significantly boosting demand for secondary and tertiary paper packaging products such as corrugated boxes, paper bags, and protective wraps. As digital retail continues to grow, the need for durable, lightweight, and sustainable shipping packaging is accelerating market growth.

• Versatility and Cost-Effectiveness of Paper Packaging Paper packaging is widely valued for its durability, versatility, lightweight nature, and recyclability. Available in a wide variety of shapes, sizes, and grades, it serves diverse end-use industries — from food and beverages to cosmetics and healthcare — making it one of the most universally adopted packaging solutions in the country.

• Growing Demand Across Food and Beverage Sector The food and beverage industry remains the largest end-use segment for paper packaging, driven by expanding packaged food consumption, health-conscious product labeling trends, and increasing use of liquid paperboard cartons and folding boxes for food-safe applications across retail and foodservice channels.

Get Customized Segmentation Intelligence — Speak Directly to Our Expert: https://www.imarcgroup.com/request?type=report&id=3328&flag=C

United States Paper Packaging Industry Segmentation

IMARC Group provides detailed segmentation analysis across product type, grade, packaging level, and end use industry categories, with forecasts at regional and country levels for 2026–2034.

Analysis by Product Type

- Corrugated Boxes — Leading Segment Corrugated boxes dominate the paper packaging market, serving as the backbone of e-commerce logistics, retail shipping, and industrial packaging. Their superior structural strength, stackability, and recyclability make them the preferred choice for secondary and tertiary packaging applications across virtually every industry.

- Folding Boxes and Cases Folding cartons are widely used in food, pharmaceutical, and personal care packaging. Their printability and customization flexibility make them ideal for retail shelf presentation and brand identity communication.

- Liquid Paperboard Cartons Liquid paperboard cartons are a high-growth segment, driven by rising consumption of dairy products, juices, and plant-based beverages. Their barrier properties and sustainable profile make them a preferred alternative to plastic and glass containers.

- Paper Bags and Sacks Paper bags and sacks are experiencing a resurgence as retailers and brands phase out single-use plastic bags in compliance with regulatory mandates and consumer preferences for eco-friendly alternatives.

- Others This includes wrapping paper, tissue packaging, molded fiber products, and specialty paper packaging formats for industrial and agricultural use.

Analysis by Grade

- Solid Bleached

- Coated Recycled

- Uncoated Recycled

- Others

Coated recycled grades are gaining traction as manufacturers prioritize post-consumer recycled content to meet sustainability targets, while solid bleached boards remain preferred for premium food and healthcare packaging requiring high-quality print surfaces.

Analysis by Packaging Level

- Primary Packaging — Direct product contact packaging such as cartons, bags, and wraps.

- Secondary Packaging — Outer packaging for grouping and retail display, including folding cases.

- Tertiary Packaging — Bulk transport packaging such as corrugated boxes and pallet wraps.

Analysis by End Use Industry

- Food — Dominant Segment The food industry accounts for the largest share of paper packaging demand, supported by the widespread use of corrugated boxes, paperboard cartons, and bags across fresh produce, bakery, frozen food, and packaged grocery segments.

- Beverages Liquid paperboard cartons and paper-based multipack carriers are key formats in the beverage segment, particularly for dairy, juice, and ready-to-drink categories.

- Personal Care and Home Care Premium folding cartons and retail-ready packaging formats are widely used in personal care and home care for brand differentiation and sustainable positioning on retail shelves.

- Healthcare Healthcare packaging relies on paper-based solutions for pharmaceutical cartons, medical device packaging, and sterile wrapping materials, driven by safety, traceability, and regulatory compliance requirements.

- Others This includes retail, electronics, agriculture, and industrial end-use applications.

Regional Spotlight: Where Is Growth Concentrated?

South — Market Leader The South region holds the largest share of the U.S. paper packaging market, supported by a robust manufacturing base, high concentration of food processing facilities, and strong retail and e-commerce distribution infrastructure across major hubs like Dallas, Houston, Atlanta, and Charlotte.

West — Sustainability and Innovation Hub The West, particularly California, is a leading region for sustainable packaging innovation, driven by some of the most progressive state-level plastic ban regulations in the country. High consumer environmental awareness and a strong tech-enabled retail ecosystem are fueling demand for premium paper packaging formats.

Northeast — High-Value Urban Demand The Northeast benefits from dense urban populations, high consumer spending power, and a strong retail and foodservice sector. Cities like New York, Boston, and Philadelphia are key demand centers for branded folding cartons and premium packaging solutions in the personal care and food segments.

Midwest — Industrial and Agricultural Strength The Midwest is a stable growth region supported by its strong agricultural and food processing industries, which drive consistent demand for paper bags, sacks, and corrugated boxes for bulk transport and distribution. Expanding e-commerce fulfillment networks are also adding incremental demand across the region.

Future Scope: What Lies Ahead for the U.S. Paper Packaging Market?

• Accelerating Shift Away from Single-Use Plastics As regulatory pressure intensifies at the federal and state levels, the transition from plastic to paper-based packaging is expected to accelerate across all end-use industries. This structural shift presents significant long-term growth opportunities for paper packaging manufacturers and converters.

• Innovation in Barrier and Functional Paper Packaging Advancements in barrier coating technologies are enabling paper packaging to replace plastic in moisture-sensitive, grease-resistant, and temperature-controlled applications. Next-generation functional paper packaging will expand addressable markets in fresh food, frozen food, and liquid categories.

• Growth of Recycled and Post-Consumer Content Packaging Rising corporate sustainability commitments and consumer preference for circular economy solutions will drive increased adoption of packaging made from recycled paper fiber. Investment in recycled content supply chains and certification programs is expected to intensify throughout the forecast period.

• E-Commerce Packaging Optimization As online retail continues to grow, demand for right-sized, frustration-free, and lightweight corrugated packaging solutions will rise. Brands will increasingly invest in custom-designed paper packaging that enhances the unboxing experience while reducing material waste and shipping costs.

• Strategic Consolidation and Capacity Expansion Major paper packaging manufacturers are expected to pursue acquisitions, partnerships, and greenfield capacity expansions to meet growing demand and improve supply chain resilience. Investment in automated manufacturing and digital printing technologies will further differentiate leading players in the competitive landscape.

Frequently Asked Questions (FAQ)

1.What is the current size of the United States paper packaging market?

The U.S. paper packaging market was valued at USD 84.2 Billion in 2025.

2. What is the projected value of the market by 2034?

The market is expected to reach USD 98.9 Billion by 2034, driven by rising sustainability mandates, e-commerce growth, and expanding demand across food, beverage, and healthcare sectors.

3. What is the expected CAGR of the U.S. paper packaging market?

The market is projected to grow at a CAGR of 1.80% during 2026–2034.

4. Which region dominates the U.S. paper packaging market?

The South region currently leads the market, supported by a large manufacturing base, strong food processing industry presence, and well-developed retail and logistics infrastructure.

5. What are the key growth drivers of the U.S. paper packaging market?

Major growth drivers include rising environmental concerns, government regulations promoting eco-friendly packaging, the surge in e-commerce activity, growing demand from the food and beverage industry, and increasing consumer preference for recyclable and sustainable packaging solutions.

About IMARC Group

IMARC Group is a leading global market research company providing data-driven insights and expert consulting services to businesses seeking to achieve their strategic objectives. With a multi-disciplinary team of industry experts, IMARC delivers thorough, reliable market intelligence across sectors including Chemicals and Materials, Healthcare, Technology, Agriculture, Retail, and more.

Contact

IMARC Group

Email: sales@imarcgroup.com

United States: +1–201–971–6302

India: +91–120–433–0800

United Kingdom: +44–753–714–6104

Join our community to interact with posts!