According to insights from IMARC Group, the United States influenza diagnostics market is witnessing steady growth due to increasing seasonal influenza outbreaks, rising awareness regarding early disease detection, and continuous advancements in diagnostic technologies. Influenza diagnostics play a crucial role in identifying viral infections quickly and accurately, enabling healthcare providers to initiate timely treatment and prevent the spread of the disease across communities. The growing focus on outbreak monitoring and pandemic preparedness is also strengthening the demand for advanced diagnostic solutions across hospitals, laboratories, and home-based testing environments.

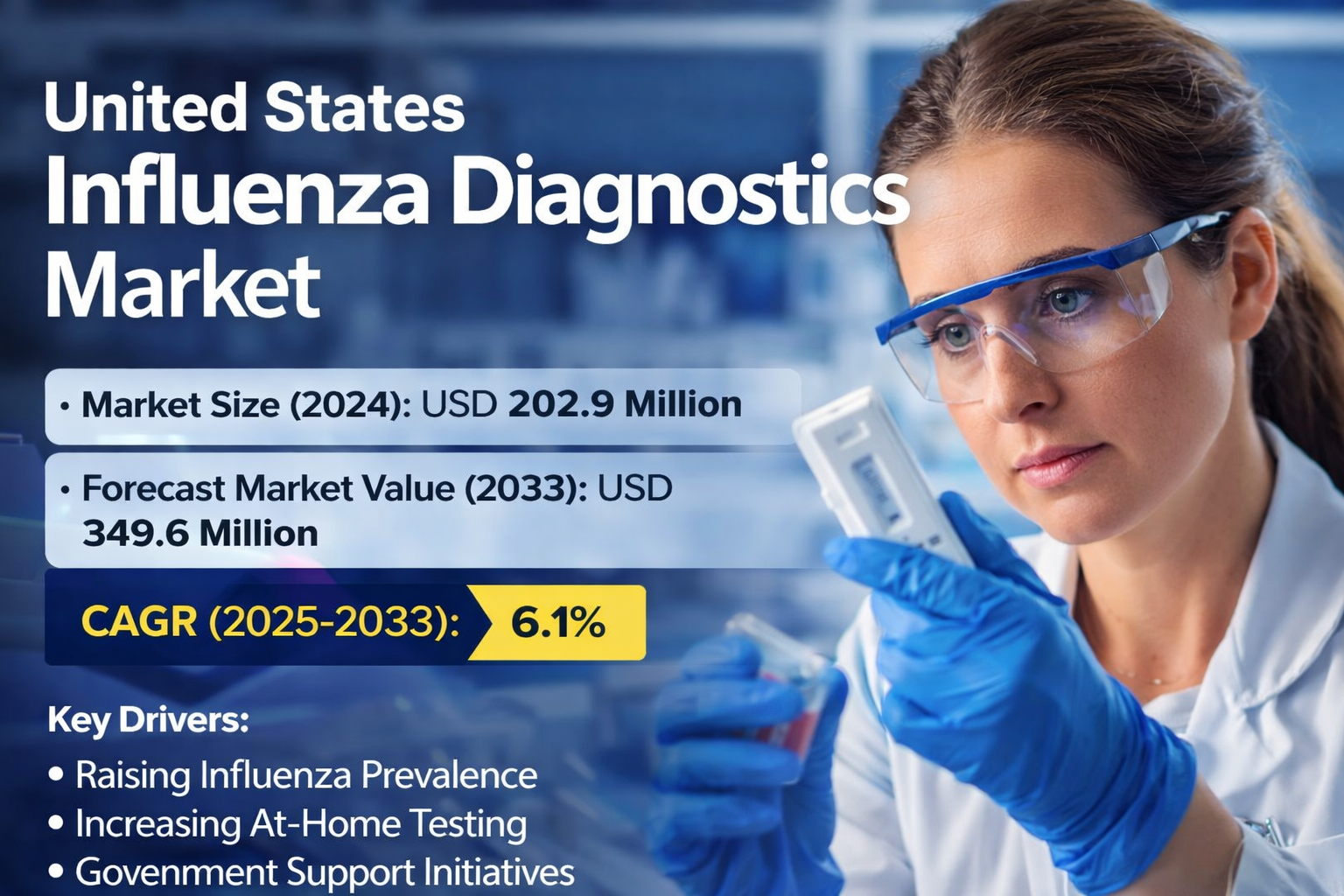

The United States influenza diagnostics market size was valued at USD 202.9 Million in 2024 and is projected to reach USD 349.6 Million by 2033, exhibiting a compound annual growth rate (CAGR) of 6.1% during 2025–2033. Market growth is supported by increasing healthcare investments, widespread use of rapid testing technologies, expanding government initiatives, and continuous research collaborations aimed at improving influenza detection and management strategies.

United States Influenza Diagnostics Market Key Statistics

• Market Size (2024): USD 202.9 Million

• Forecast Market Value (2033): USD 349.6 Million

• CAGR (2025–2033): 6.1%

• Base Year: 2024

• Historical Years: 2019–2024

• Forecast Years: 2025–2033

Key Takeaways from the United States Influenza Diagnostics Market

• Increasing seasonal influenza outbreaks are significantly boosting demand for accurate and rapid diagnostic testing solutions.

• Government initiatives aimed at improving healthcare accessibility are expanding diagnostic testing infrastructure across the country.

• Strategic partnerships between diagnostic companies and public health agencies are accelerating innovation in testing technologies.

• Growing consumer preference for at-home diagnostic kits is transforming the influenza testing landscape.

• Continuous investments in vaccine development and surveillance programs are strengthening influenza detection capabilities.

• Rising awareness among healthcare professionals about early testing protocols is improving diagnostic accuracy and disease management.

United States Influenza Diagnostics Market Growth Drivers: Rising Flu Incidence and Demand for Early Detection

The increasing prevalence of seasonal influenza remains one of the most significant drivers of the United States influenza diagnostics market. According to the Centers for Disease Control and Prevention (CDC), the 2023–2024 influenza season resulted in approximately 40 million illnesses, 18 million medical visits, 470,000 hospitalizations, and nearly 28,000 deaths across the country. These statistics highlight the importance of rapid and reliable diagnostic tools for early disease detection and outbreak control.

Early diagnosis enables healthcare providers to initiate timely antiviral treatment, reducing the severity of symptoms and preventing further transmission of the virus. As influenza continues to affect millions of individuals annually, healthcare systems are increasingly prioritizing diagnostic testing as part of broader disease management strategies.

Another factor supporting market growth is the increasing number of older adults in the United States. Elderly populations are more vulnerable to severe influenza complications, prompting healthcare providers to emphasize targeted diagnostic testing to ensure timely treatment and improved patient outcomes.

Strategic collaborations between government agencies and private diagnostic companies are also accelerating innovation in testing technologies. For instance, on February 15, 2024, the Biomedical Advanced Research and Development Authority (BARDA) partnered with BioFire Defense, LLC through a USD 13 Million contract to develop the Emerging Flu Panel (EFP). This advanced diagnostic solution is designed to identify influenza A, influenza B, and emerging influenza viruses within 60 minutes, strengthening the nation’s pandemic preparedness capabilities.

United States Influenza Diagnostics Market Trends: Government Initiatives Expanding Diagnostic Accessibility

Government initiatives are playing a significant role in improving access to influenza diagnostic tools across the United States. Federal and state health agencies are implementing programs aimed at distributing rapid diagnostic technologies and providing training for healthcare professionals to ensure accurate testing practices.

In October 2024, the U.S. Food and Drug Administration (FDA) authorized the Healgen Rapid Check COVID-19/Flu A&B Antigen Test, an over-the-counter diagnostic solution designed for quick and convenient influenza detection. The test provides results within 15 minutes using a simple nasal swab and demonstrated high accuracy levels, including 99.9% accuracy in identifying negative influenza A and influenza B samples.

Government subsidies for diagnostic equipment are also supporting healthcare providers in underserved rural and urban communities. By improving access to rapid testing solutions in pharmacies, clinics, and community health centers, these initiatives help ensure early disease detection and effective management of influenza outbreaks.

United States Influenza Diagnostics Market Trends: Growing Adoption of At-Home Testing Kits

Consumer demand for convenient healthcare solutions has led to a significant rise in the adoption of at-home influenza diagnostic kits. These testing solutions allow individuals to perform rapid antigen tests from home, reducing the need for hospital visits while enabling faster identification of influenza infections.

In October 2024, BARDA partnered with Revvity, Inc. through a USD 9.2 Million agreement to develop a molecular at-home testing platform capable of detecting influenza A, influenza B, and SARS-CoV-2. The platform features a reusable hub and disposable testing cartridge and provides results within 30 minutes with minimal user interaction.

The growing availability of home testing kits through pharmacies and online retail channels is further accelerating their adoption. These solutions are particularly attractive to tech-savvy consumers seeking quick, reliable, and convenient diagnostic options for monitoring respiratory illnesses.

United States Influenza Diagnostics Market Trends: Increasing Investments in Advanced Vaccine Development

Rising investments in advanced influenza vaccine technologies are also contributing to the growth of the influenza diagnostics market. Pharmaceutical companies are increasingly investing in innovative vaccine development platforms to improve immunogenicity and accelerate vaccine production timelines.

For example, in March 2024, Moderna secured a USD 750 Million funding agreement with Blackstone Life Sciences to advance the development of next-generation influenza vaccines using mRNA technology. These investments aim to improve vaccine effectiveness by enabling faster adaptation to evolving influenza strains.

The focus on advanced vaccine research is closely linked to the need for accurate diagnostic tools that can identify circulating influenza strains. By supporting surveillance programs and early detection efforts, influenza diagnostics play a crucial role in guiding vaccine development and public health strategies.

United States Influenza Diagnostics Market Segmentation Insights

By Product

• Test Kit and Reagents: These products are essential for identifying influenza viruses quickly and accurately. Enhanced reagents improve the sensitivity and specificity of diagnostic tests, enabling healthcare providers to manage outbreaks more effectively.

• Instruments: Diagnostic instruments such as PCR systems and immunoassay analyzers allow laboratories to process large sample volumes efficiently. These tools ensure precise detection of viral RNA and support high-throughput testing.

• Others: Additional diagnostic tools and consumables support influenza detection and laboratory workflows.

By Test Type

• Molecular Diagnostic Tests: These include PCR-based assays and isothermal nucleic acid amplification tests capable of detecting influenza viral RNA with high accuracy.

• Traditional Diagnostic Tests: Rapid influenza diagnostic tests (RIDTs), viral culture tests, fluorescent antibody tests, and serological tests provide quick results and remain widely used in outpatient settings.

By Type of Flu

• Type A Flu: This strain is the most significant contributor to influenza outbreaks and pandemics, making it a primary focus for diagnostic testing.

• Type B Flu: Although generally less severe than Type A, Type B influenza contributes to seasonal outbreaks and requires accurate detection for proper treatment.

• Type C Flu: This strain typically causes mild respiratory illness but remains important in comprehensive diagnostic assessments.

By End User

• Hospitals: Hospitals serve as primary testing centers for severe influenza cases and play a vital role in monitoring outbreaks.

• Diagnostic Laboratories: Laboratories provide specialized testing services using advanced molecular diagnostic technologies.

• Others: Additional testing environments include clinics, research institutions, and community health facilities.

By Region

• Northeast: High population density and colder winters increase influenza transmission, making diagnostic testing essential.

• Midwest: The region’s climate and mixed urban-rural population drive demand for accessible diagnostic solutions.

• South: The large population and higher prevalence of chronic diseases increase the need for early influenza detection.

• West: Innovation in biotechnology and diagnostic technologies supports the development of advanced influenza testing tools.

United States Influenza Diagnostics Market Competitive Landscape

The United States influenza diagnostics market remains highly competitive as companies continue to develop advanced testing technologies to improve diagnostic accuracy and speed. Diagnostic manufacturers are focusing on rapid molecular testing solutions, integrated diagnostic platforms, and innovative at-home testing kits to meet evolving healthcare demands.

Collaborations between diagnostic companies, research institutions, and public health agencies are also strengthening the development of next-generation diagnostic tools. For instance, Quest Diagnostics secured contracts from the CDC in October 2024 to develop diagnostic tests targeting H5 avian influenza and the Oropouche virus, ensuring readiness for potential outbreak scenarios and supporting national public health preparedness initiatives.

Recent Updates and Key Developments:

- On October 10, 2024, Emory University in Atlanta introduced new over-the-counter combination tests capable of detecting influenza A, influenza B, and COVID-19 using a single nasal swab. These tests provide a fast and convenient option for individuals to identify the cause of respiratory symptoms at home. Dr. Greg Martin, a lead researcher at ACME POCT, highlighted that these tests play a crucial role in enabling timely treatment decisions during peak respiratory virus seasons.

- On October 30, 2024, the U.S. Department of Agriculture (USDA) implemented enhanced testing and monitoring protocols for H5N1 avian influenza to protect both livestock and public health. The new approach features a tiered milk sample collection system to detect the virus effectively, supporting improved biosecurity and containment measures. This initiative is expected to boost demand for advanced diagnostic tools and stimulate innovation in the United States influenza diagnostics market.

Frequently Asked Questions (FAQs)

Q1. What is the size of the United States influenza diagnostics market?

The market reached USD 202.9 Million in 2024.

Q2. What is the forecast value of the market by 2033?

The market is expected to reach USD 349.6 Million by 2033.

Q3. What is the growth rate of the market?

The market is projected to grow at a CAGR of 6.1% during 2025–2033.

Q4. What factors drive the influenza diagnostics market in the United States?

Key drivers include rising influenza prevalence, government support for diagnostics, technological advancements, and growing adoption of at-home testing kits.

Q5. Which end users dominate the influenza diagnostics market?

Major end users include hospitals, diagnostic laboratories, and healthcare clinics.

Author IMARC Group

IMARC Group is a global management consulting firm dedicated to helping the world's most ambitious changemakers create a lasting impact. We offer a comprehensive suite of market entry and expansion services, including market assessment, feasibility studies, regulatory navigation, and strategic marketing. Our actionable insights empower clients to make informed decisions and achieve sustainable growth.

Contact Us

IMARC Group

Email: sales@imarcgroup.com

United States: +1-201-971-6302

Join our community to interact with posts!