Market Overview

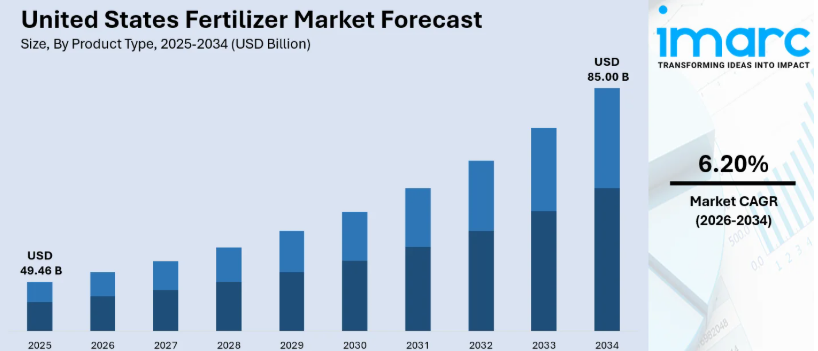

The United States fertilizer market size was valued at USD 49.46 Billion in 2025 and is projected to reach USD 85.00 Billion by 2034, growing at a compound annual growth rate (CAGR) of 6.20% from 2026 to 2034. This growth is driven by expanding agricultural production demands, increased adoption of precision farming techniques, and the growing need for enhanced crop yields. Additionally, sustainable agricultural practices and supportive government policies for domestic productivity and food security further propel market expansion.

Study Assumption Years

-

Base Year: Not provided in source

-

Historical Year/Period: 2020-2025

-

Forecast Year/Period: 2026-2034

United States Fertilizer Market Key Takeaways

-

Current Market Size: USD 49.46 Billion in 2025

-

CAGR: 6.20%

-

Forecast Period: 2026-2034

-

Chemical fertilizer dominates the market with an 83% share in 2025, due to nutrient specificity and economical nature.

-

Straight fertilizers lead with a 57% share in 2025, offering targeted nutrient delivery at affordable costs.

-

Dry form fertilizer holds 68% market share in 2025, driven by improved storage stability and compatibility with traditional equipment.

-

Grains and cereals dominate crop type segment with 40% share in 2025, fueled by large-scale corn, wheat, and soybean production.

-

The South region leads with a 30% share in 2025, supported by varied agricultural practices and year-round growing seasons.

Sample Request Link: https://www.imarcgroup.com/united-states-fertilizer-market/requestsample

Market Growth Factors

The escalating global food demand compels the United States to enhance agricultural productivity continuously, positioning fertilizers as essential inputs. Growth in population and dietary shifts toward protein-rich food increase pressure on agricultural systems to maximize outputs from arable lands. Farmers are adopting intensified production and optimized fertilization strategies to maintain food security and export competitiveness, driving sustained investment in fertilizer applications across diverse crops.

The rise of precision agriculture technologies fundamentally reshapes fertilizer application. By December 2024, about 68% of large U.S. crop farms had adopted precision agriculture tools, including yield monitors and soil maps, enabling field-specific nutrient management. These technologies promote efficient fertilizer use, reduce waste, and improve crop nutrient uptake, encouraging wider adoption of both conventional and specialty fertilizers.

Government initiatives supporting domestic agriculture also drive market growth. Policies addressing farm income stability, conservation, and research foster productive land management that includes optimized fertilization. Technical assistance programs facilitate nutrient management aligned with environmental stewardship. The regulatory balance between productivity and environmental concerns promotes innovation of fertilizers that meet performance and sustainability criteria.

Market Segmentation

-

**Product Type:**

-

Chemical Fertilizer

-

Biofertilizers

Chemical fertilizers have broad market dominance due to their proven effectiveness in improving yields, concentrated nutrient content, and standardized formulations that allow precise application.

-

**Product:**

-

Straight Fertilizers

-

Nitrogenous Fertilizers

-

Urea

-

Calcium Ammonium Nitrate

-

Ammonium Nitrate

-

Ammonium Sulfate

-

Anhydrous Ammonia

-

Others

-

Phosphatic Fertilizers

-

Mono-Ammonium Phosphate (MAP)

-

Di-Ammonium Phosphate (DAP)

-

Single Super Phosphate (SSP)

-

Triple Super Phosphate (TSP)

-

Others

-

Potash Fertilizers

-

Muriate of Potash (MoP)

-

Sulfate of Potash (SoP)

-

Secondary Macronutrient Fertilizers

-

Calcium Fertilizers

-

Magnesium Fertilizers

-

Sulfur Fertilizers

-

Micronutrient Fertilizers

-

Zinc

-

Manganese

-

Copper

-

Iron

-

Boron

-

Molybdenum

-

Others

-

Complex Fertilizers

Straight fertilizers represent 57% of the market in 2025 and provide versatility in addressing specific nutrient deficiencies. They enable customized nutrient programs based on soil testing, benefiting farming operations with precise and cost-effective nutrient management.

-

**Product Form:**

-

Dry

-

Liquid

Dry fertilizers hold 68% share due to advantages in storage stability, handling, compatibility with spreading equipment, and improved application quality through continual manufacturing enhancements.

-

**Crop Type:**

-

Grains and Cereals

-

Pulses and Oilseeds

-

Fruits and Vegetables

-

Flowers and Ornamentals

-

Others

Grains and cereals dominate with a 40% share, reflecting their nutrient-intensive nature and prominence across the Midwest and Great Plains, requiring multiple nutrient applications throughout growth stages.

-

**Region:**

-

Northeast

-

Midwest

-

South

-

West

The South leads the market with a 30% share in 2025, attributed to favorable climate, extended growing seasons, diverse crop cultivation, and developed infrastructure enabling year-round intensive farming.

Regional Insights

The South region leads the United States fertilizer market with a 30% share in 2025, supported by warm climatic conditions allowing multiple cropping cycles annually. The area's diverse crop production and adequate rainfall sustain continuous and varied fertilizer demand. Infrastructure development in the South enhances distribution efficiency and timely product availability for critical application periods.

Speak To An Analyst:https://www.imarcgroup.com/request?type=report&id=19951&flag=C

Recent Developments & News

In August 2024, Itafos, a North American fertilizer multinational, announced an expansion in Brazil by opening a new office in Luís Eduardo Magalhães, Bahia. This strategic move aims to increase regional sales from 20% to 30% by 2025, strengthen relationships with farmers, and leverage local grain production alongside strategic logistics to improve competitive positioning.

Key Players

-

CF Industries Holdings, Inc.

-

Haifa Group

-

ICL Group Ltd.

-

Koch Industries Inc.

-

Nutrien Ltd.

-

Sociedad Química y Minera de Chile SA

-

The Andersons Inc.

-

The Mosaic Company

-

Wilbur-Ellis Company LLC

-

Yara International ASA

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us

IMARC Group,

134 N 4th St. Brooklyn, NY 11249, USA,

Email: sales@imarcgroup.com,

Tel No: (D) +91 120 433 0800,

United States: +1-201971-6302

Join our community to interact with posts!