Global Automotive Split-View Camera Module Market Valued at USD 23.80 Billion in 2025, Projected to Excel Beyond USD 48 Billion by 2032 Amid Intensifying ADAS Integration and Global Safety Mandates

An elite global business intelligence, automotive vertical analysis, and engineering consulting corporation, has officially launched its highly comprehensive, data-backed industry study on the Global Automotive Split-View Camera Module Market (Report Code: 309031). The exhaustive research publication offers an authoritative evaluation of next-generation automotive perception systems, outlining critical structural growth drivers, software-defined vision platforms, regional manufacturing shifts, and strategic enterprise roadmaps across advanced mobility industries.

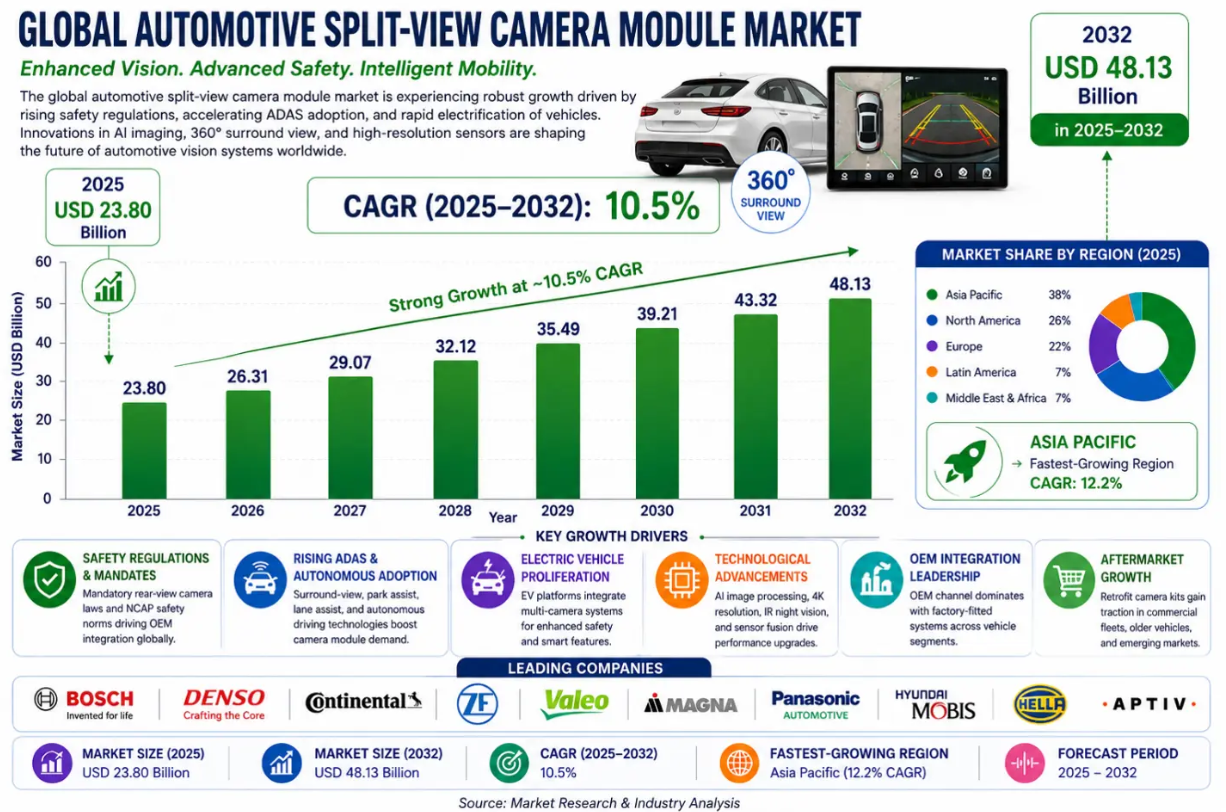

The intensive market study demonstrates that the global automotive split-view camera module sector stands at the absolute center of the contemporary vehicle safety and automated driving evolution. Valued at USD 23.80 Billion in 2025, the market is tracking toward an estimated valuation of USD 48.13 Billion by 2032, expanding at an extraordinary Compound Annual Growth Rate (CAGR) of 10.58% during the forecast period. This remarkable growth trajectory represents a fundamental shift in vehicle architecture: as automotive design moves rapidly toward higher levels of autonomy and Software-Defined Vehicles (SDVs), multi-angle split-view camera modules have transitioned from an optional luxury convenience to a mandatory, high-volume production component.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/309031/

Executive Summary: Eliminating Low-Speed Blind Zones Through Multi-Angle Perception Integration

Modern urban environments, dense traffic corridors, and large vehicle footprints have pushed standard mirror-based and single-perspective automotive visibility to its practical limits. Operating large passenger vehicles, delivery vans, and heavy freight trucks in restricted spaces introduces severe commercial liabilities, driving up minor collision frequencies and insurance claim expenditures. Traditional single-lens rear or front cameras present a limited, fixed field of view that fails to capture low-side obstacles, cross-traffic hazards, and blind-zone intersections.

The automotive split-view camera module architecture solves these visibility challenges by using wide-angle lenses (typically featuring a field of view ranging from 120° to 190°) coupled with real-time digital image segmentation. Instead of feeding a single static image to the interior display, a split-view system captures multi-angle footage simultaneously and processes the data through centralized electronic control units (ECUs). This allows the vehicle to display stitched surround perspectives, concurrent side-and-rear views, and cross-traffic overlays on the infotainment screen, improving driver situational awareness and near-field object recognition.

The granular intelligence report analyzes the global automotive split-view camera module market structure across several key categories to provide maximum clarity for industry stakeholders:

-

By Lens Type & Resolution: Standard Resolution Modules (1.3 MP to 2 MP), High-Definition Modules (5 MP to 8 MP+), Wide-Angle Fisheye Lenses, and Multi-Lens Sensor Configurations.

-

By Camera View & Application: Rear-View Split Systems, Front Cross-Traffic View Modules, Side-Mirror Replacement Cameras, and 360-Degree Surround View Systems.

-

By Technology Integration: Basic Split Display Systems, AI-Enabled Image Processing Modules (featuring edge-detection and motion tracking), and Integrated ADAS Sensor Systems.

-

By Installation Type & Sales Channel: Factory-Integrated OEM Solutions and Commercial Retrofit Kits/Aftermarket Standalone Modules.

-

By Vehicle Type: Passenger Vehicles (Compact, Mid-Size, Premium, and Luxury Sport Utility Vehicles), Light Commercial Vehicles (LCVs), and Heavy Commercial Vehicles (HCVs).

Core Market Dynamics: Primary Economic, Regulatory, and Autonomous Growth Drivers

An analytical review of the global automotive electronics space highlights several structural economic and technical forces that are accelerating enterprise capital expenditure (CapEx) for split-view camera module deployment.

1. Evolving Global Safety Mandates and New Car Assessment Programs (NCAP)

Government-imposed safety regulations represent the most powerful structural driver for the automotive split-view camera module market. Following the landmark rear-visibility mandates in the United States, the European Union's updated General Safety Regulation (GSR) has mandated advanced reversing detection and blind-spot monitoring systems for all new vehicle platforms.

Concurrently, regional New Car Assessment Programs (such as Euro NCAP and China NCAP) continue to raise the engineering benchmarks required to secure coveted 5-star safety ratings. To satisfy these evolving criteria—particularly regarding vulnerable road user (VRU) protection and pedestrian detection during low-speed maneuvers—automotive manufacturers are standardizing multi-camera, split-view perception envelopes across both premium and mass-market vehicle trims.

2. Accelerating Deployment of Level 2+ and Level 3 ADAS Architectures

The rapid development and commercialization of advanced driver-assistance systems are profoundly reshaping the demand profile for optical camera modules. Level 2+ and Level 3 automated driving systems, which encompass automated parking assist, highway pilot functions, and proactive collision avoidance, rely on a constant stream of high-resolution visual data.

Split-view camera modules are integral to the sensor fusion architectures that combine camera, radar, and lidar inputs. Rather than acting as passive displays for the driver, modern split-view modules feed high-frequency image data directly into autonomous driving stacks, providing the precise edge detection and proximity assessment required for automated vehicle positioning.

3. Transition Toward Software-Defined Vehicles and Domain Controller Consolidation

Historically, automotive camera architectures used fragmented, point-to-point wiring systems where each camera operated independently. The industry transition toward Software-Defined Vehicles (SDVs) has accelerated the adoption of centralized domain electronic control units. High-speed serialization protocols, such as Gigabit Multimedia Serial Link (GMSL2), allow a single central processing unit to capture and interpret multiple high-resolution split-view camera streams simultaneously. This consolidation dramatically reduces in-vehicle wiring weight, lowers assembly complexity, and enables manufacturers to deploy over-the-air (OTA) software updates that continuously improve image processing algorithms and feature options.

Technical Segment Analysis: Identifying High-Value Automotive Channels

Passenger Vehicles Command the Majority Share of Revenue Volume

By vehicle type, the Passenger Vehicles segment dominates the global market, accounting for over 72.5% of total demand. While initial deployment was restricted to premium luxury sedans and high-end SUVs, the entry-level and mid-range passenger vehicle segments are experiencing fast adoption rates as component costs decline. SUVs and modern pickup trucks represent a high-value niche within passenger vehicles; their extended body profiles and elevated blind spots make multi-angle split-view systems and predictive path overlays essential for parking and towing maneuvers.

AI-Enabled Image Processing Systems Reflect Hyper-Growth Trajectories

By technology integration, AI-Enabled Image Processing Systems and Integrated ADAS Camera Modules are outperforming basic split display components. Basic systems that merely display raw, unedited camera feeds are being replaced by intelligent camera modules equipped with embedded vision processors. These next-generation systems do not just show the environment; they actively interpret it—providing real-time hazard highlighting, moving object detection (MOD), and dynamic stitching adjustments that alter the display perspective based on steering wheel angles and vehicle speed.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/309031/

Regional Developments: Advanced Safety Hubs and High-Velocity Manufacturing Zones

North America: High-Value Fleet Optimization and Towing Integration

North America holds a leading position in the global market, driven by consumer demand for large-format vehicles, light trucks, and long-haul commercial transport. In the United States, approximately 78% of the light vehicle sales mix consists of SUVs and pickup trucks, which directly increases the per-vehicle camera installation rate. The market focus in this region centers on high-resolution module integration, custom towing assistant software, and cross-traffic warning systems designed to manage large vehicles in tight urban logistics hubs.

Asia-Pacific: The Dominant, High-Velocity Global Production Engine

The Asia-Pacific (APAC) region represents the largest and fastest-growing market for automotive split-view camera modules, controlling a substantial 39.6% revenue share. This leading regional market presence is anchored by high vehicle production volumes and advanced automotive electronics ecosystems in China, Japan, South Korea, and India.

Taiwanese and Chinese manufacturing hubs dominate the global supply of optical lenses and image sensors, while Japanese safety car initiatives incentivize domestic OEMs to integrate comprehensive multi-camera setups. The rapid expansion of electric vehicle (EV) manufacturing in APAC serves as a primary catalyst, as EV developers use advanced multi-view camera technology as a key product differentiator.

Competitive Intelligence: Strategic Imperatives of Market Leaders

The global automotive split-view camera module market features an intensive, high-stakes competitive environment where tier-1 automotive suppliers, optical component specialists, and semiconductor designers invest heavily in product innovation.

Key industry participants analyzed within the comprehensive market report include:-

1. Robert Bosch GmbH.

2.Continental AG.

3.ZF Friedrichshafen AG,

4Valeo S.A.,

5.Magna International Inc.

6.Denso Corporation,

7.Ficosa International S.A.

8.Aptiv PLC.

9.Panasonic Holdings Corporation.

10.Intel Corporation (Mobileye).

11Ambarella, Inc.

The primary competitive strategies used by these industry leaders center on enhancing optical resolution, reducing low-light latency, and expanding software capabilities:

-

Next-Generation Sensor Integration: Market leaders are transitioning from traditional 1.2-megapixel sensors to advanced 8-megapixel configurations, providing the high image clarity required for both driver visualization and long-range machine vision algorithms.

-

Turnkey Domain Architectures: Tier-1 suppliers like Bosch and Continental are designing unified vision processing platforms that package split-view camera modules directly with centralized ADAS domain controllers, simplifying validation for global OEMs.

-

Advanced Optical Coatings: Providers are investing heavily in innovative hydrophobic, anti-icing, and self-cleaning lens coatings to ensure reliable multi-angle camera performance under adverse weather conditions like heavy rain or snow.

For full access to the comprehensive strategic report, visit:https://www.maximizemarketresearch.com/market-report/automotive-split-view-camera-module-market/309031/

Industry Bottlenecks: Managing Thermal Dissipation and Environmental Resistance

Despite solid growth, the widespread implementation of advanced automotive camera modules requires overcoming specific engineering and operational challenges.

The primary engineering challenge for split-view camera modules is environmental durability. Because these modules are mounted on exposed areas like front grilles, side mirrors, and trunk lids, they must withstand extreme conditions. They are subjected to constant thermal cycling, stone chips, road salt, and high-pressure washing. Ensuring long-term optical alignment and moisture sealing requires sophisticated packaging materials and expensive manufacturing processes.

Additionally, managing high-definition video data streams introduces data transmission challenges. Relaying multiple uncompressed video feeds to a central processor requires high-speed, low-latency links. Any dropped frames or processing lag can compromise the safety of integrated ADAS features, making strict timing validation essential during system development.

Strategic Outlook: The Transition to High-Fidelity Digital Mirrors and Glass Substrates

Looking forward, the global automotive split-view camera module market is positioned to expand beyond traditional assistant configurations. The next phase of automotive vision innovation will be defined by the commercial adoption of High-Fidelity Digital Side-Mirror Replacements. By swapping bulky physical side mirrors for aerodynamic split-view camera pods, automakers can reduce aerodynamic drag, improve vehicle range, and provide drivers with wide-angle views that dynamically adjust during lane changes and reversing maneuvers.

Furthermore, processing chips are integrating advanced neural networks directly into the camera housing. This edge-AI design allows individual modules to process and compress visual information locally, reducing the computing load on the central vehicle ECU. For automotive executives, product planners, and technology directors, investing in flexible, high-resolution split-view architecture is critical for maintaining product relevance. Implementing standard-compliant, AI-driven vision solutions today ensures that vehicle platforms remain compatible with future autonomous driving requirements.

About Maximize Market Research

Maximize Market Research is a multifaceted market research and consulting company with professionals from several industries. Some of the industries we cover include medical devices, pharmaceutical manufacturers, science and engineering, electronic components, industrial equipment, technology and communication, cars and automobiles, chemical products and substances, general merchandise, beverages, personal care, and automated systems. To mention a few, we provide market-verified industry estimations, technical trend analysis, crucial market research, strategic advice, competition analysis, production and demand analysis, and client impact studies.

Contact Maximize Market Research

3rd Floor, Navale IT Park, Phase 2

Pune Bangalore Highway, Narhe,

Pune, Maharashtra 411041, India

sales@maximizemarketresearch.com

+91 96071 95908, +91 9607365656

Join our community to interact with posts!