When it comes to protecting financial systems, AML policies play a crucial role. Financial institutions in New York City face some of the most stringent regulations in the country, making it vital to implement effective measures. Whether you are a bank, a fintech startup, or a money services business, having the right compliance framework in place helps you stay ahead of risks and avoid costly penalties.

The financial sector is highly dynamic in New York, NY, with thousands of transactions occurring every minute. This makes the city a prime target for illicit money flows if preventive steps are not taken. That is where strong AML measures come into play. These policies are not just a regulatory requirement; they are a shield against fraud, terrorist financing, and other financial crimes.

Why AML Policies Matter for Financial Institutions

AML policies are the backbone of a financial institution’s compliance system. They define the rules, workflows, and monitoring mechanisms that ensure suspicious activities are flagged and reported in time. For businesses in New York, NY, adopting a robust compliance culture is not optional, it is mandatory. Regulators like the Financial Crimes Enforcement Network (FinCEN) and the New York State Department of Financial Services (NYDFS) expect institutions to implement effective frameworks to safeguard the financial ecosystem.

In practical terms, these policies help:

-

Detect unusual transactions

-

Prevent money laundering and terrorist financing

-

Ensure compliance with federal and state regulations

-

Build trust with clients and regulators

Without a proper plan in place, financial institutions risk heavy fines, reputational damage, and even license revocation.

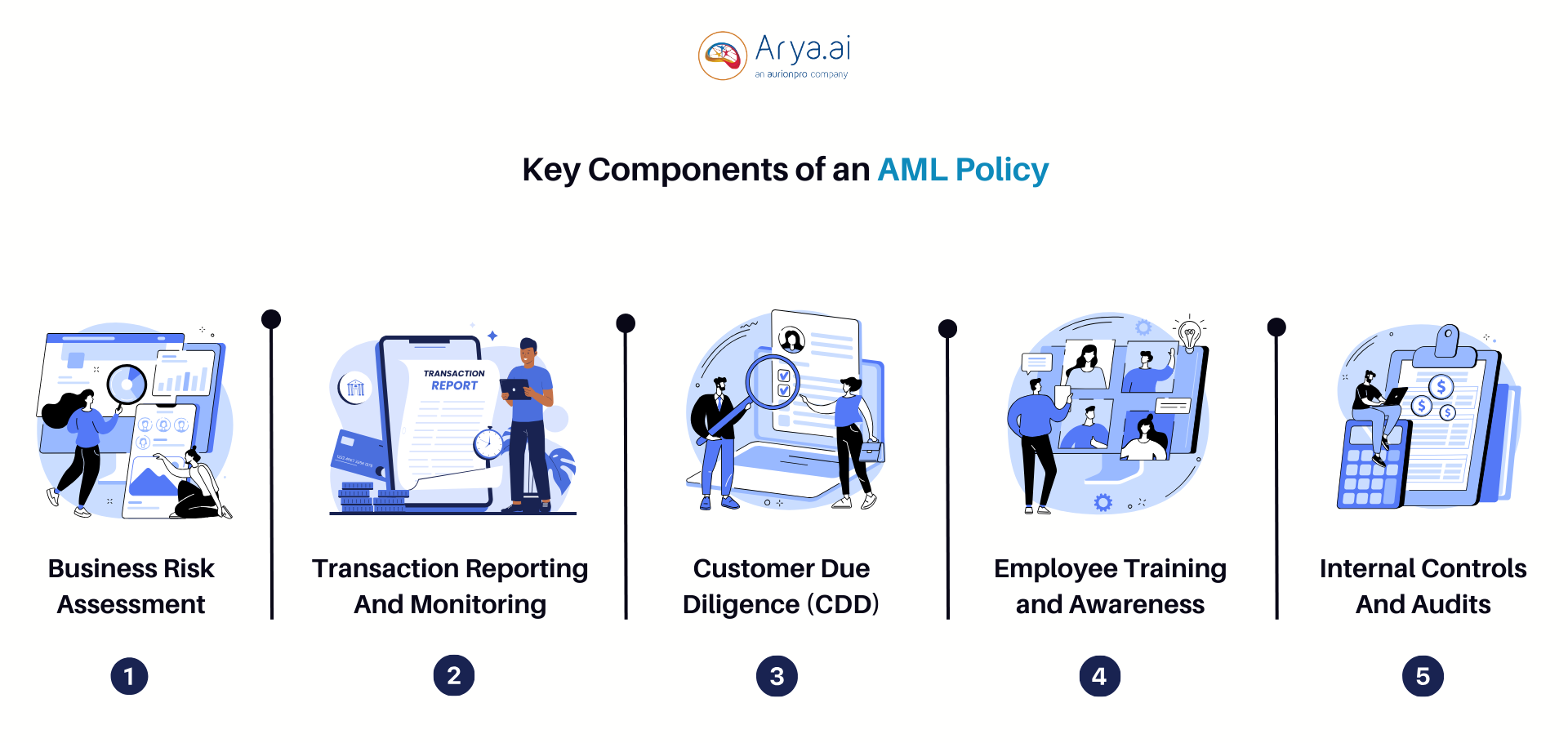

Key Components of Strong AML Policies

To create the best AML policies, financial institutions need to focus on certain key elements:

1. Risk Assessment

Before drafting any framework, it is essential to understand the type of risks your organization faces. Banks, investment firms, and payment processors deal with different customer profiles and transaction volumes. A thorough risk assessment helps you decide what level of monitoring and controls are necessary.

2. Customer Due Diligence (CDD)

This process ensures you know your customers before allowing them to use your services. Verifying identity documents, understanding the source of funds, and categorizing clients based on risk levels are all part of CDD. Enhanced due diligence should be applied to high-risk clients to avoid exposure to illicit activities.

3. Transaction Monitoring

A solid AML compliance program includes monitoring systems that can identify suspicious activities in real-time. This could involve automated alerts for unusual transaction sizes, frequency, or patterns that deviate from normal behavior.

4. Reporting and Recordkeeping

Regulations require financial institutions to file Suspicious Activity Reports (SARs) whenever a red flag is detected. Proper recordkeeping ensures that the institution can provide evidence of compliance during regulatory audits.

5. Staff Training

Even the best systems will fail if employees are not aware of their responsibilities. Regular training sessions should be conducted to educate staff about recognizing suspicious behavior and following escalation procedures.

Building an Effective AML Program

The ideal compliance setup is not just about meeting regulatory requirements it’s about creating a culture of vigilance. Institutions must develop internal policies that are easy to follow and integrate seamlessly into daily operations. Technology plays a vital role here, as advanced software solutions can automate monitoring, risk scoring, and reporting.

Working with a trusted AML company or consultant can also make implementation easier, especially for smaller financial firms. They can help design customized solutions that fit your business model while remaining cost-effective.

Best Practices for Financial Institutions

Here are some actionable tips to strengthen your compliance efforts:

-

Conduct periodic reviews of your AML framework to keep it up to date with changing regulations.

-

Leverage data analytics to identify patterns and emerging risks.

-

Encourage employees to report potential issues without fear of retaliation.

-

Test your systems regularly to ensure they are functioning as intended.

Institutions like FinGuru360 New York, NY have shown that proactive measures significantly reduce risks and help maintain long-term compliance.

Conclusion

The financial industry continues to evolve, and so do the risks. The best way to protect your institution is by adopting strong AML policies and procedures that match the unique risk environment of your business. Investing in a comprehensive AML program today will save you from regulatory headaches tomorrow. If you are looking for reliable AML solutions, partnering with experts can streamline your compliance journey and keep your operations secure.

FAQs

1. What are AML policies?

AML policies are a set of rules and procedures that financial institutions follow to detect and prevent money laundering and other illegal financial activities.

2. Why are AML policies important?

They protect businesses from financial crimes, help maintain regulatory compliance, and build trust with customers and authorities.

3. Who needs AML policies?

Any business involved in financial transactions banks, fintechs, money service businesses, and investment firms should have them in place.

4. How often should AML policies be updated?

They should be reviewed at least annually or whenever there are significant changes in regulations or your business operations.

5. Can small businesses implement AML programs?

Yes, small businesses can implement simplified frameworks that match their size and risk profile, often with the help of compliance consultants.

Join our community to interact with posts!