Automotive Clutch Market Overview

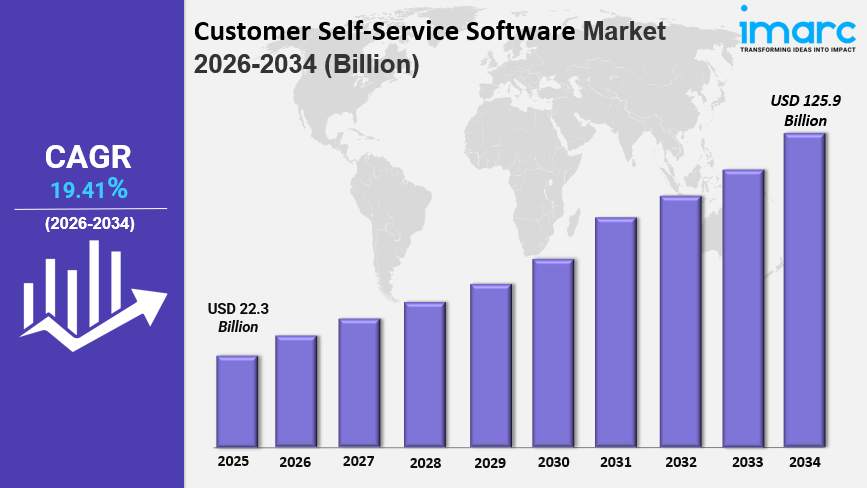

The global automotive clutch market is on a steady growth trajectory, driven by increasing demand for commercial and passenger vehicles worldwide, rising adoption of advanced transmission technologies, and stringent emission and fuel economy regulations. Valued at USD 14.3 Billion in 2025, the market is projected to reach USD 21.1 Billion by 2034, exhibiting a CAGR of 4.20% during 2026–2034. Growth is powered by innovations in dual-clutch transmissions, the rise of electric and hybrid vehicles requiring specialized clutch systems, evolving automated manual transmission (AMT) technologies, and increasing investments in R&D by leading manufacturers.

Access In-Depth Market Intelligence — Download Your Free Sample Copy: https://www.imarcgroup.com/automotive-clutch-market/requestsample

Key Market Statistics at a Glance

- Base Year: 2025

- Historical Years: 2020–2025

- Forecast Period: 2026–2034

- Market Size (2025): USD 14.3 Billion

- Projected Size (2034): USD 21.1 Billion

- Growth Rate: CAGR of 4.20%

- Leading Region: Asia Pacific (Largest market in 2025)

Global Automotive Clutch Market Growth Trends

Improvements in Clutch Systems and Technology Continuous technological advancements in clutch design are significantly contributing to market growth. In October 2023, Clutch Industries introduced UniClutch — a patented, adaptable system engineered to boost torque capacity without compromising drivability. Similarly, in January 2024, Schaeffler India showcased its latest dual-clutch and automated manual transmission offerings at the SIAT Expo in Pune. Manufacturers are also prioritizing optimal production line management and strict quality control systems, with new product introductions such as TERBON's high-performance clutch kit in April 2024 underscoring the industry's commitment to durability and long-term performance.

Increasing Demand for Electric and Hybrid Vehicles The global shift toward electric vehicles (EVs) is reshaping clutch technology requirements. Since EVs utilize single-speed transmission systems that bypass traditional clutch mechanisms, manufacturers are innovating next-generation clutch systems that can seamlessly integrate with electric powertrains. In April 2024, Magna developed advanced all-wheel drive systems alongside dual-clutch transmissions tailored for hybrid applications. In May 2024, GM filed a patent for a modular clutch actuation system designed specifically for EV transmissions. In March 2024, Zero introduced a simulated clutch system for electric motorcycles, reflecting the growing emphasis on specialized solutions for alternative-powered vehicles.

Stringent Emission Regulations and Regulatory Support Regulatory authorities across the globe are enforcing increasingly strict vehicle emission and efficiency standards, compelling automotive manufacturers to adopt advanced clutch technologies that reduce environmental impact. The U.S. NHTSA and EPA have implemented extended light-duty vehicle standards that are expected to catalyze market innovation. Government bodies are additionally encouraging lightweight material adoption in clutch manufacturing, with high-performance examples such as carbon ceramic clutch systems highlighting the industry's material innovation trajectory.

Rising Vehicle Production and Expanding Automotive Industry Inflating living standards globally are propelling vehicle sales for both personal and commercial use, directly expanding the demand for automotive clutches. The growing preference for manual and automated manual transmissions — particularly in emerging markets — is acting as a key growth-inducing factor. Countries across Asia, Latin America, and the Middle East are witnessing accelerated vehicle production, sustaining a strong pipeline of clutch demand across both OEM and aftermarket channels.

Development of Automated Manual Transmission (AMT) Technologies The development and rapid adoption of AMT technologies is emerging as one of the defining trends of the global automotive clutch market. AMT systems combine the fuel economy benefits of manual transmissions with the convenience of automatic gear shifting, making them attractive for both passenger vehicle and commercial vehicle applications. Key players including Schaeffler India and Valeo are investing heavily in AMT and DCT development, reinforcing this segment's contribution to overall market expansion.

Get Customized Segmentation Intelligence — Speak Directly to Our Expert: https://www.imarcgroup.com/request?type=report&id=1486&flag=C

Global Automotive Clutch Industry Segmentation

IMARC Group provides detailed segmentation analysis across vehicle type, transmission type, clutch type, clutch disk/plate size, distribution channel, and material type, with forecasts at global and regional levels for 2026–2034.

Analysis by Vehicle Type

- Passenger Vehicles — Leading Segment Passenger vehicles account for the largest share of the automotive clutch market. Growing global demand for personal transportation, coupled with automaker investment in diverse clutch technologies — from single-plate dry clutches in compact cars to dual-clutch transmissions in performance vehicles — underpins this segment's dominance. The shift toward hybrid and electric passenger vehicles is further driving demand for innovative clutch architectures.

- Commercial Vehicles Commercial vehicles represent a significant and growing segment, particularly in markets with expanding freight, logistics, and construction industries. Heavy-duty clutches with enhanced durability and vapor management characteristics are critical for long-haul trucks, buses, and off-road commercial applications.

Analysis by Transmission Type

- Manual Transmission — Leading Segment Manual transmission continues to hold the largest market share, driven by strong consumer preference among driving enthusiasts, lower manufacturing and maintenance costs, and robust adoption across commercial and off-road vehicles in both developed and emerging markets.

- Automatic Transmission Automatic transmissions are gaining ground globally, particularly in premium passenger vehicle segments and urban markets where convenience and driving comfort take priority over manual engagement.

- Automated Manual Transmission (AMT) AMT is one of the fastest-growing transmission segments, combining the mechanical efficiency of manual systems with the ease of automation. It is rapidly gaining popularity in both light commercial vehicles and entry-level passenger cars across price-sensitive markets.

- Others This category encompasses continuously variable transmissions (CVTs), dual-clutch transmissions (DCTs), and other advanced hybrid powertrain configurations.

Analysis by Clutch Type

- Friction Clutch — Leading Segment Friction clutches dominate the market due to their versatility, reliability, and widespread adoption across manual transmission systems. From everyday passenger cars to high-performance vehicles such as the Ford Mustang and Chevrolet Camaro, friction clutches deliver the smooth power transfer and durability required across a broad range of driving conditions.

- Dog Clutch Dog clutches are favored for their precise and direct engagement in motorsport, racing, and specialized off-road applications where speed of gear change is prioritized over smooth engagement.

- Hydraulic Clutch Hydraulic clutches are gaining traction in heavy commercial vehicles and high-performance passenger vehicles, offering superior modulation, reduced pedal effort, and consistent performance under demanding operating conditions.

- Others This includes electromagnetic clutches and centrifugal clutches used in specialized industrial and automotive applications.

Analysis by Clutch Disk/Plate Size

- Below 9 Inches — Leading Segment Clutches measuring below 9 inches account for the largest market share, driven by the growing global popularity of compact vehicles, city cars, and motorcycles that prioritize lightweight design, agility, and fuel efficiency. Models like the Fiat 500 and Honda CBR series exemplify this segment's widespread application.

- 9 Inches to 10 Inches This mid-range size category serves standard passenger vehicles and light-duty commercial applications, balancing torque handling capability with space efficiency within vehicle drivetrains.

- 10 Inches to 11 Inches Larger clutch sizes in this range are deployed in mid-sized commercial vehicles and performance passenger cars that require greater torque capacity and enhanced thermal management.

- 11 Inches and Above The largest clutch sizes are essential for heavy commercial vehicles, long-haul trucks, and industrial machinery where maximum torque transmission, durability, and heat dissipation are non-negotiable requirements.

Analysis by Distribution Channel

- OEM — Leading Segment OEM channels hold the largest market share, with leading suppliers such as Valeo, EXEDY Corporation, and ZF Friedrichshafen providing precision-engineered clutch systems directly to major automakers including Ford, Toyota, and BMW. OEM partnerships ensure seamless integration, strict regulatory compliance, and optimal performance characteristics in new vehicles.

- Aftermarket The aftermarket segment serves vehicle maintenance, repair, and performance upgrade needs. Growing vehicle parc sizes, increasing average vehicle age, and rising consumer interest in performance upgrades are collectively supporting sustained aftermarket demand globally.

Analysis by Material Type

- Ceramic — Leading Segment Ceramic clutches hold the largest material segment share, valued for their exceptional heat resistance, high durability, and consistent performance under extreme conditions. They are widely used in high-performance sports cars such as the Porsche 911 GT3 and Chevrolet Corvette Z06, as well as in heavy-duty and off-road applications.

- Organic Organic clutches remain widely used in standard passenger vehicles and light commercial applications due to their smooth engagement characteristics and cost-effectiveness.

- Others This includes carbon composite and metallic clutch materials adopted in specialized racing, motorsport, and industrial powertrain applications.

Regional Spotlight: Where Is Growth Concentrated?

Asia Pacific — Market Leader Asia Pacific dominates the global automotive clutch market, driven by the region's expansive automotive industry, rising disposable incomes, and surging vehicle production. China — the world's largest automotive market — generates enormous clutch demand through manufacturers like BYD and Geely. In India, domestic automakers such as Maruti Suzuki and Tata Motors sustain a high-volume clutch supply requirement. Japanese OEMs including Toyota and Honda continue to drive demand for advanced clutch technologies, while regional clutch manufacturers like EXEDY Corporation and FCC Co., Ltd. reinforce Asia Pacific's supply-side dominance.

Europe — Second-Largest Market Europe is a major automotive clutch market, anchored by the world's second-largest vehicle production base. Countries like Germany, France, and Italy are key production hubs. The region's stringent emissions regulations and strong consumer preference for fuel-efficient vehicles — including hybrids and EVs — are accelerating demand for advanced clutch technologies. Strategic industry collaborations, such as the Aisin Seiki-Tohoku Magnet Institute motor technology partnership announced in May 2023, are shaping next-generation clutch development across the continent.

North America — Innovation and Regulatory-Driven Growth North America is a significant market characterized by the presence of major automotive manufacturers and a robust consumer demand for diverse vehicle types. The U.S. regulatory framework — including NHTSA and EPA emission and efficiency standards — is driving investment in cleaner and more advanced clutch technologies. The growing adoption of hybrid vehicles and performance-oriented passenger cars is also sustaining demand for premium clutch solutions across the region.

Latin America — Rising Automotive Production Brazil and Mexico are the primary growth drivers in Latin America. Brazil's expanding domestic automotive sector and Mexico's status as a major OEM manufacturing hub — with over 351,000 light vehicles produced in November 2024 alone — are generating consistent demand for clutch systems. As vehicle production volumes rise, the need for high-quality and durable clutch solutions will continue to amplify across the region.

Middle East and Africa — Growing Vehicle Fleet Saudi Arabia's automotive market, with approximately 8 million passenger cars and over 650,000 new vehicle sales annually, anchors clutch demand across the Middle East and Africa region. Rapid urbanization, infrastructure expansion, and a growing middle class across the broader region are supporting steady fleet growth, directly translating into increased demand for both OEM and aftermarket clutch solutions.

Future Scope: What Lies Ahead for the Global Automotive Clutch Market?

EV-Compatible and Hybrid Clutch Innovation As electrification accelerates across global automotive markets, clutch manufacturers will invest significantly in developing specialized systems for hybrid and electric powertrains. Innovative products such as GM's modular EV clutch actuation system and Zero's simulated clutch for electric motorcycles signal the direction of R&D investment through 2034. Manufacturers that develop scalable, EV-compatible clutch architectures will gain a decisive competitive advantage.

Dual-Clutch Transmission (DCT) Expansion The growing consumer preference for vehicles that deliver both fuel efficiency and dynamic performance is expected to sustain strong demand for DCT-equipped vehicles. Automakers and clutch suppliers are investing in next-generation DCT systems that offer faster gear shifts, reduced energy losses, and compatibility with hybrid powertrains — positioning DCT as a high-growth product category through the forecast period.

Lightweight Material Innovation Ongoing pressure to reduce vehicle weight and meet emissions targets will drive further adoption of advanced materials such as carbon composites, ceramic compounds, and lightweight alloys in clutch manufacturing. Industry leaders like McLaren — whose P1 features a carbon ceramic clutch system — demonstrate the market direction, as weight reduction remains central to automaker performance and sustainability strategies.

Aftermarket Growth and Service Ecosystem Expansion As the global vehicle parc continues to grow and the average age of vehicles increases, aftermarket demand for clutch replacement and performance upgrades will expand steadily. Digital commerce platforms and the professionalization of vehicle servicing networks in emerging markets will further enhance aftermarket accessibility, providing a durable revenue stream for clutch suppliers.

Strategic Partnerships and R&D Investment Key players are expected to deepen strategic collaborations to accelerate clutch technology innovation. Cross-industry partnerships — such as those between clutch manufacturers and transmission system developers — will foster integrated powertrain solutions that enhance vehicle performance, fuel efficiency, and compliance with evolving global emission standards throughout the forecast period.

Frequently Asked Questions (FAQ)

1. What is the current size of the global automotive clutch market?

The global automotive clutch market was valued at USD 14.3 Billion in 2025.

2. What is the projected value of the market by 2034?

The market is expected to reach USD 21.1 Billion by 2034, driven by rising vehicle production, EV and hybrid adoption, and continuous advancements in clutch technologies.

3. What is the expected CAGR of the automotive clutch market?

The market is projected to grow at a CAGR of 4.20% during 2026–2034.

4. Which region dominates the global automotive clutch market?

Asia Pacific currently leads the market, supported by the region's expansive automotive manufacturing base, rising vehicle sales, and the presence of leading clutch manufacturers in countries such as Japan, China, India, and South Korea.

5. What are the key growth drivers of the global automotive clutch market?

Major growth drivers include increasing global vehicle production, stringent emission and fuel economy regulations, rising adoption of EV and hybrid vehicles necessitating specialized clutch systems, technological advancements in DCT and AMT, and growing demand for lightweight and high-performance clutch materials.

6. Which vehicle type holds the largest share in the market?

Passenger vehicles currently hold the largest share, reflecting robust global demand for personal transportation and automaker investment in diverse clutch technologies across vehicle categories.

7. Who are the leading companies in the global automotive clutch market?

Key players include Aisin Seiki Co., Ltd., Schaeffler Group, ZF Friedrichshafen AG, BorgWarner Inc., Valeo, EXEDY Corporation, Eaton Corporation Inc., F.C.C. Co. Ltd., Magneti Marelli S.p.A., Allison Transmission Inc., and FTE Automotive GmbH, among others.

About

IMARC Group is a leading global market research company providing data-driven insights and expert consulting services to businesses seeking to achieve their strategic objectives. With a multi-disciplinary team of industry experts, IMARC delivers thorough, reliable market intelligence across sectors including Chemicals and Materials, Healthcare, Technology, Agriculture, Retail, and more.

Contact

IMARC Group

Email: sales@imarcgroup.com

United States: +1–201–971–6302

India: +91–120–433–0800

United Kingdom: +44–753–714–6104

Join our community to interact with posts!