The biopharmaceutical sector is witnessing a paradigm shift as the focus moves toward high-precision safety testing. Central to this evolution is the Residual DNA Testing Market Share, which is expanding as manufacturers prioritize the removal of host cell contaminants from biological products. With the complexity of modern therapies increasing, the ability to quantify trace amounts of genetic material has become a cornerstone of pharmaceutical quality assurance.

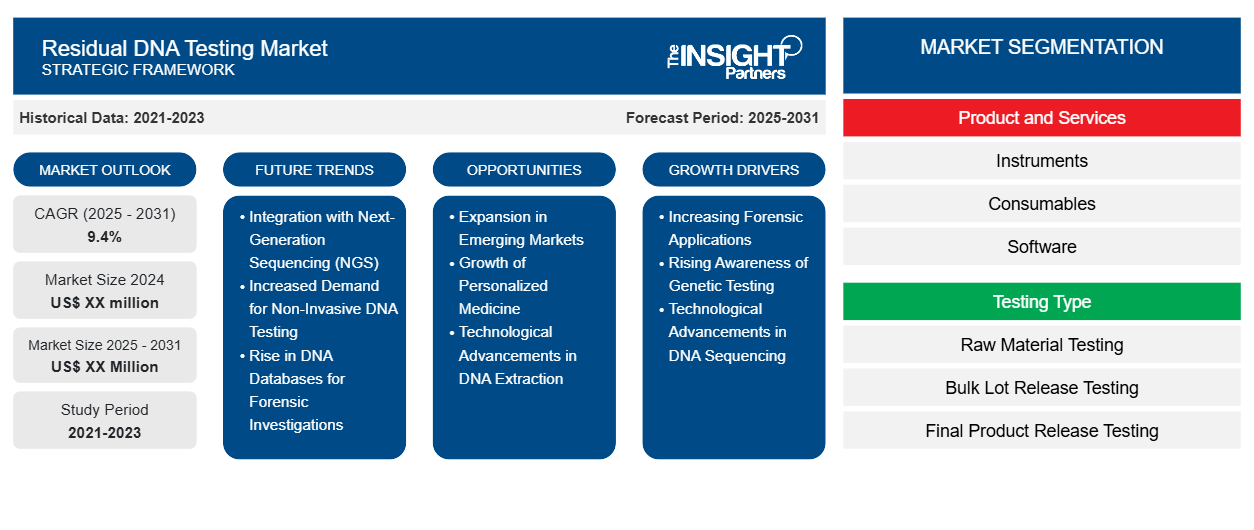

The Residual DNA Testing Market is expected to register a CAGR of 9.4% from 2025 to 2031. This growth is underpinned by the massive influx of biosimilars entering the clinical pipeline and the rapid commercialization of viral vector-based treatments. As the industry matures, the Residual DNA Testing Market Share is becoming increasingly concentrated among providers who can offer high-sensitivity assays that meet the rigorous standards of modern pharmacopeias.

Download Sample Report - https://www.theinsightpartners.com/sample/TIPRE00040891

Primary Market Report Drivers

The expansion of the Residual DNA Testing Market Share is primarily propelled by the following drivers:

- Stringent Regulatory Compliance: Regulatory bodies like the FDA and EMA have established strict limits—often below 100 pg per dose—for residual host cell DNA. Failure to meet these benchmarks can lead to clinical holds or product recalls, making advanced testing an absolute necessity.

- Surge in Cell and Gene Therapies (CGT): Unlike traditional biologics, CGT products involve intricate genetic engineering. The risk of oncogenic DNA sequences or infectious agents makes residual DNA testing a high-stakes requirement for these modalities.

- Shift Toward Quantitative PCR (qPCR) and NGS: The transition from older, less sensitive hybridization methods to qPCR and Next-Generation Sequencing (NGS) is a major driver. These technologies provide the speed and precision required for high-throughput manufacturing environments.

- Rising Outsourcing to CDMOs: Many pharmaceutical firms are now outsourcing their testing needs to Contract Development and Manufacturing Organizations (CDMOs). This shift is centralizing the Residual DNA Testing Market Share within specialized service providers that possess the latest analytical instrumentation.

Top Players and Competitive Landscape

The competitive environment is defined by a commitment to innovation and the development of standardized, "ready-to-use" kits that minimize variability. The following top players are instrumental in driving the Residual DNA Testing Market Share forward:

- Thermo Fisher Scientific Inc.

- Merck KGaA (MilliporeSigma)

- Agilent Technologies, Inc.

- Bio-Rad Laboratories, Inc.

- QIAGEN

- F. Hoffmann-La Roche Ltd.

- Promega Corporation

- Charles River Laboratories

- Eurofins Scientific

- Sartorius AG

- Takara Bio Inc.

- Lonza Group AG

Forecast and Opportunities Through 2031

By 2031, the Residual DNA Testing Market Share is expected to see a significant boost from emerging economies, particularly in the Asia Pacific region. As China and India solidify their roles as biomanufacturing hubs, the demand for localized, cost-effective testing solutions will soar. Furthermore, the integration of digital PCR (dPCR) into routine testing protocols offers a new frontier for growth, providing absolute quantification without the need for standard curves.

The future of the market lies in automation. Reducing the manual labor involved in sample preparation not only lowers costs but also significantly decreases the risk of cross-contamination, a critical factor when dealing with the ultra-low detection limits required today.

Related Report:

Hospital-Acquired Disease Testing Market Analysis and Forecast by Size, Share, Growth, Trends 2031

Contact Information -

Email: sales@theinsightpartners.com

Phone: +1-646-491-9876

Join our community to interact with posts!