Global Automotive Glass Market Poised to Reach USD 39.30 Billion by 2032, Driven by EV Proliferation, Smart Glazing Innovations, and Stringent Consumer Safety Mandates

A leading global business intelligence and strategic consulting firm, has released its comprehensive, data-driven industry report titled "Global Automotive Glass Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032."

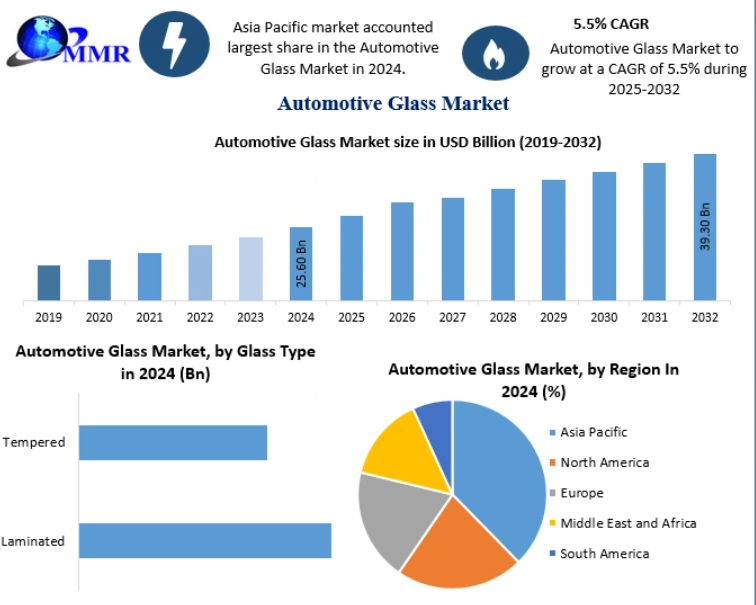

The study highlights a major transformation within the global automotive supply chain. Valued at a robust USD 25.60 Billion in 2024, the global automotive glass market is projected to expand at a steady compound annual growth rate (CAGR) of 5.5% during the forecast period from 2025 to 2032, ultimately culminating in a market valuation of approximately USD 39.30 Billion by 2032.

This sustained expansion is primarily catalyzed by architectural shifts in vehicle designs, surging global production of electric vehicles (EVs) and hybrid vehicles, a growing consumer appetite for high-end luxury features such as panoramic sunroofs, and the integration of next-generation smart glass technologies. Furthermore, rigid automotive crash-safety standards implemented by international regulatory bodies are compelling original equipment manufacturers (OEMs) to transition from conventional safety glass to high-performance laminated and specialized acoustic glass architectures.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/16890/

Understanding the Structural Evolution of Modern Automotive Glass

Automotive glass has evolved from a basic structural windshield designed to shield passengers from wind and debris into a highly technical, multi-functional component critical to vehicle structural integrity, thermal regulation, aerodynamics, and digital user interfaces. Modern automotive glass is a specialized form of processed float glass that undergoes intense thermal, mechanical, and chemical tempering processes. This toughening workflow yields glass units capable of withstanding intense external impact pressures, structural stress, and dramatic thermal variances.

Beyond standard structural reinforcement, modern glazing materials are engineered to include advanced chemical formulations that reject infrared (IR) and ultraviolet (UV) radiation. This specific performance characteristic prevents solar heat from penetrating the vehicle cabin, reducing the load on HVAC systems and improving the fuel economy of Internal Combustion Engine (ICE) vehicles and the battery range of electric platforms. Additionally, advanced acoustic interlayer technologies dramatically reduce ambient road noise, creating a quieter, more premium interior cabin experience.

Primary Market Dynamics: What is Fueling Global Industry Expansion?

1. The Global Surging Demand for Electric and Hybrid Vehicles

The global automotive landscape is undergoing a historic transition toward sustainable mobility, heavily incentivized by government mandates aimed at cutting carbon emissions. As battery-electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs) capture greater market share, the demand for specialized, high-performance automotive glass has escalated.

In 2024, global EV sales grew substantially, with approximately 14.2 million new pure electric and plug-in hybrid vehicles delivered globally—representing a 35% year-over-year increase. Out of these, 10 million were pure battery-electric vehicles (BEVs). China continues to lead this shift, serving as both the largest consumer market and production hub, accounting for 8.4 million units and roughly 59% of global EV sales in 2024. In the United States, EV and hybrid markets continue to gain traction, backed by massive legislative framework investments such as the Infrastructure Investment and Jobs Act (allocating USD 7.5 billion toward domestic fast-charging networks) and the Inflation Reduction Act, which extends consumer tax credits of up to USD 7,500 for qualifying electric vehicles through 2032.

For glass manufacturers, the rise of electric vehicles shifts engineering requirements. EVs require lightweight materials to optimize driving ranges, forcing glass manufacturers to develop ultra-thin, highly robust laminated glass segments that reduce vehicle weight without compromising passenger protection.

2. The Integration of Smart Glass and Advanced Glazing Technologies

Smart glass represents the future of automotive glazing architecture. Research and development investments are flowing into active and passive smart glass variants capable of dynamic light transmission alteration. One major application of this tech is the integration of Head-Up Displays (HUDs), turning the vehicle windshield into a digital interactive dashboard reminiscent of a modern aircraft flight deck.

By projecting critical telemetry data—such as navigation directions, current velocity, and real-time safety alerts—directly onto the glass surface, HUD-enabled windshields reduce driver distraction and enhance overall safety. Furthermore, the adoption of electronically switchable suspended particle devices (SPDs) and polymer-dispersed liquid crystal (PDLC) technology allows occupants to adjust glass tint at the press of a button, boosting thermal comfort and privacy. This integration of smart tech is expected to considerably lift the per-unit value of automotive glass across the forecast window.

3. Growth of the Global Luxury and High-End Automotive Segment

Rising disposable incomes, high standards of living, rapid urbanization, and lifestyle changes have triggered a worldwide surge in luxury vehicle sales. For example, India’s luxury car market reached a record high of 42,731 units registered in 2024, demonstrating a notable 20% year-over-year growth. Major premium manufacturers like BMW, Mercedes-Benz, and Audi are noting steady demand increases driven by corporate earnings, economic recoveries, and younger professionals entering the premium segment.

Luxury vehicles rely heavily on advanced glass installations to establish brand differentiation. Features such as multi-pane panoramic sunroofs, expansive ambient glass roofs, and acoustic side laminated windows are standard offerings in high-end segments. Companies like Tesla, Ferrari, and Volvo have expanded their usage of panoramic laminated glass configurations to build sleek, modern vehicle aesthetics, which in turn drives overall glass consumption per vehicle.

Regulatory Environments and Crash-Safety Optimization

International government interventions serve as a structural backbone for the automotive glass market. Safety regulations implemented by organizations like the National Highway Traffic Safety Administration (NHTSA) in the United States and the European New Car Assessment Programme (Euro NCAP) enforce rigid performance parameters for occupant crash protection.

Windshields play a foundational role in vehicle safety, providing up to 30% of a vehicle's structural cabin strength during rollover accidents and acting as the primary backstop for passenger-side airbag deployments. Additionally, strict government zero-emission vehicle (ZEV) programs—along with laws in various global jurisdictions mandating the phase-out of traditional internal combustion engines by 2035—are encouraging manufacturers to streamline vehicle aerodynamics. Sleek, sweeping glass angles reduce drag coefficients, improving aerodynamic efficiency and aligning with environmental mandates.

Industry Constraints: Capital Density and Technical R&D Roadblocks

Despite strong growth trajectories, the global automotive glass market faces certain manufacturing challenges. The primary obstacle is the requirement for substantial initial capital investments and ongoing research and development costs. Producing high-performance automotive glass—specifically thin, lightweight laminated glass configurations for side and rear applications—demands sophisticated, specialized thermal manufacturing plants and precise chemical tempering machinery.

Furthermore, integrating advanced glass layers with electrochromic or HUD technologies adds complexity to production lines, elevating manufacturing costs. In cost-sensitive developing economies, the high replacement and upfront purchase costs of smart or laminated glass limit adoption rates, leaving basic tempered alternatives as the standard option for entry-level vehicles. Navigating these production complexities and minimizing cost burdens for consumers remain core challenges for industry participants.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/16890/

Comprehensive Segment Insights

Analysis by Glass Type: Lamination Dominates the Windshield Ecosystem

Based on glass type, the market is segmented into Laminated Glass and Tempered Glass. The laminated glass segment held the majority market share in 2024 and is expected to maintain its dominance throughout the forecast period.

Laminated glass is manufactured by sandwiching an advanced plastic interlayer, typically Polyvinyl Butyral (PVB), between two or more layers of high-grade float glass. This structural combination yields excellent safety profiles: upon high-velocity impact, the glass cracks but fragments adhere firmly to the internal PVB interlayer, reducing the risk of flying glass shards striking passengers. This characteristic makes laminated glass the legally mandated choice for front windshields globally.

On the other hand, tempered glass undergoes quick cooling processes that cause it to break into small, blunt pieces rather than sharp shards. It remains highly utilized across side windows and rear backlights due to its mechanical strength and cost-efficiency, being four to five times stronger than basic untreated float glass.

Analysis by Vehicle Type: Passenger Vehicles Leading the Charge

By vehicle type, the market is categorized into Passenger Cars and Commercial Vehicles/Trucks. Passenger cars surpassed all other segments in 2024 to emerge as the primary volume driver. This segment is projected to grow at an individual volume CAGR of 4.3% through 2032.

This growth is supported by expanding middle-class demographics in emerging economies, urban migration patterns, and widespread auto financing options. While commercial trucks continue to lead flat volume registrations in specific heavy logistics markets—such as the United States, where truck and fleet platforms dominate rural transportation infrastructure—the high volume of passenger vehicle production ensures it remains the primary consumer of advanced automotive glass.

Regional Analysis: Evaluating Major Market Geographies

-

Asia-Pacific: The Asia-Pacific region stands as the dominant production and consumption engine for the global automotive glass market. Driven by China, Japan, India, and South Korea, the region benefits from massive manufacturing facilities, lower labor costs, and robust domestic vehicle demand. China’s dual role as the largest global EV production hub and a major exporter ensures a steady supply of automotive glass to international markets. Concurrently, India's expanding automotive sector and rising consumer purchasing power make it a high-growth market for premium automotive glass solutions.

-

North America: The North American market, led by the United States, is characterized by steady vehicle replacements, fleet modernizations, and high adoption rates of advanced driver-assistance systems (ADAS) integrated into vehicle windshields. Large consumer preferences for SUVs, light trucks, and crossovers—which utilize larger glass surface areas compared to traditional sedans—sustain strong revenue streams for glass processors across the continent.

-

Europe: Europe remains a highly innovative hub for automotive glass engineering. Driven by strict European Union carbon emission reduction targets and crash safety metrics, European premium OEMs continuously collaborate with glass manufacturers to implement lightweight glazing systems, acoustic insulation glass, and integrated solar control windows.

Strategic Recommendations and Market Insights for Stakeholders

To remain competitive in an evolving marketplace, automotive glass manufacturers, raw material suppliers, and tier-1 OEM providers should focus on strategic agility. Upgrading existing glass production infrastructures to support thin-glass lamination will be key to meeting the weight-reduction demands of global EV platforms.

Additionally, forming collaborative development partnerships with consumer electronics providers and ADAS sensor manufacturers will help accelerate the commercialization of smart windshield configurations. Minimizing manufacturing complexities and optimizing supply chains for key inputs—such as soda ash, lime, and high-performance interlayers—can protect margins against macroeconomic volatility.

For full access to the comprehensive strategic report, visit:https://www.maximizemarketresearch.com/market-report/global-automotive-glass-market/16890/

Competitive Landscape

Automotive Glass Key players

North America

1. PPG Industries - (USA)

2. Corning - (USA)

3. Gentex Corporation - (USA)

4. LKQ Corporation - (USA)

5. Magna International Inc. - (Canada)

6. Vitro, S.A.B. de C.V. - (Mexico)

7. Guardian Industries Corporation - (USA)

Asia Pacific

8. Asahi Glass Co., Ltd. - (Japan)

9. Fuyao Glass Market Group Co., Ltd. - (China)

10. Nippon Sheet Glass Co., Ltd. - (Japan)

11. Xinyi Glass Holdings Ltd. - (China)

12. Samvardhana Motherson - (India)

13. Shenzhen Benson Automobile Glass Co., Ltd. - (China)

14. Central Glass Co., Ltd. - (Japan)

15. AGC Ltd. - (Japan)

16. NSG Group - (Japan)

Europe

17. Webasto - (Germany)

18. Pilkington Glass - (United Kingdom)

19. Glas Trösch Holding AG - (Switzerland)

20. Saint-Gobain S.A. - (France)

About Maximize Market Research

Maximize Market Research is a multifaceted market research and consulting company with professionals from several industries. Some of the industries we cover include medical devices, pharmaceutical manufacturers, science and engineering, electronic components, industrial equipment, technology and communication, cars and automobiles, chemical products and substances, general merchandise, beverages, personal care, and automated systems. To mention a few, we provide market-verified industry estimations, technical trend analysis, crucial market research, strategic advice, competition analysis, production and demand analysis, and client impact studies.

Contact Maximize Market Research

3rd Floor, Navale IT Park, Phase 2

Pune Bangalore Highway, Narhe,

Pune, Maharashtra 411041, India

sales@maximizemarketresearch.com

+91 96071 95908, +91 9607365656

Join our community to interact with posts!